SECTION 3.6: Loans

In the last section, you learned about payout annuities. In this section, you will learn about conventional loans (also called amortized loans or installment loans). Examples include auto loans and home mortgages. These techniques do not apply to payday loans, add-on loans, or other loan types where the interest is calculated up front.

One great thing about loans is that they use exactly the same formula as a payout annuity. To see why, imagine that you had $10,000 invested at a bank, and started taking out payments while earning interest as part of a payout annuity, and after 5 years your balance was zero. Flip that around, and imagine that you are acting as the bank, and a car lender is acting as you. The car lender invests $10,000 in you. Since you’re acting as the bank, you pay interest. The car lender takes payments until the balance is zero.

Suppose you borrow $1,000 at a 12% annual interest rate. Again, we assume that the account is compounded with the same frequency as we make payments unless stated otherwise.

In this example with monthly payments, we assume the 12% is compounded monthly (or 1% each month). So, you make your first $100 payment at the end of the first month. At the end of the second month, you make another $100 payment, but you also have to add 1% interest on the prior balance (in this case 1% of $1,000 = $10) making the new balance (amount owed) $910 at the end of month 2.

In general, Ending Balance = Prior Balance + 1% Interest on Prior Balance – Monthly Payment

The table below shows this process over 4 months:

| Month | Prior Balance | 1% Interest on Prior Balance | Monthly Payment | Ending Balance |

| 1 | $1,000.00 | |||

| 2 | $1,000.00 | $10.00 | $100 | $910.00 |

| 3 | $910.00 | $9.10 | $100 | $819.10 |

| 4 | $819.10 | $8.19 | $100 | $727.29 |

| And so on... | ... | ... | ... | ... |

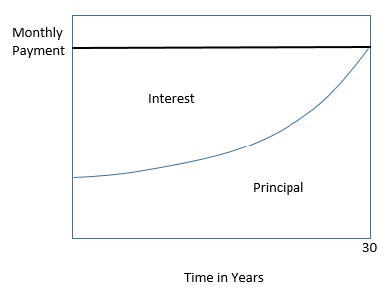

Notice that each month, the interest that must be paid decreases slightly (because you have made a payment that has decreased the principal). In an installment loan, the monthly payments are a fixed amount, so early on in the loan a larger proportion of your payment is being applied to interest, and a smaller proportion of your payment is being applied toward paying down the principal. As the term of the loan proceeds, the proportion of the payment going toward interest gradually decreases, and the proportion of the payment going toward principal gradually increases.

Example 9

You take out a 5 year installment loan to purchase a new vehicle. Your monthly payment is fixed at $485.22 for those 5 years, after which you will have paid off the loan in full. Will a larger proportion of your payment go towards principal during year 1 of the loan, or year 4 of the loan?

Solution: You owe the most money on your car when you first buy it. Since the interest due is calculated based on how much you currently owe on the loan, you owe the most interest during the first month. Keep in mind that your payment is a fixed amount, $485.22. Early in the loan, a larger proportion of your payment is going towards paying interest, while a smaller proportion of your payment is being applied to principal. As you gradually decrease your principal (the amount you owe), your interest due each month decreases as well. This means that over the life of the loan, a larger proportion of your payment can be used to pay down the principal.

Answer: During year 4 of the loan, a larger proportion of the fixed payment will go towards principal than during year 1 of the loan.

The following formula generalizes the installment loan process:

Loan Formula

P0 = [latex]\frac{PMT(1-(1+\frac{r}{n})^{-nt})}{\frac{r}{n}}[/latex]

P is the balance in the account at the beginning (starting amount, or principal).

PMT is your loan payment (your monthly payment, annual payment, etc)

r is the annual interest rate (APR) in decimal form (Example 5% = 0.05)

n is the number of compounding periods in one year.

t is the number of years we plan to borrow the money (length of the loan, in years)

Like before, the compounding frequency is not always explicitly given, but is determined by how often you make payments.

When do you use the Loan Formula?

The loan formula assumes that you make loan payments on a regular schedule (every month, year, quarter, etc.) and are paying interest on the loan.

Compound interest: One deposit

Annuity: Many deposits

Payout Annuity: Many withdrawals

Loans: Many payments

Example 10A - Algebraically

Abigale can afford $200 per month as a car payment. If she can get an auto loan at 3% interest for 60 months (5 years), how expensive of a car can she afford (in other words, what amount loan can Abigale pay off with $200 per month)?

Solution: In this example, we are looking for P0, the starting amount of the loan. Putting this into the equation:

P0 = [latex]\frac{200(1-(1+\frac{0.03}{12})^{-5(12)})}{\frac{0.03}{12}}[/latex] = $11,130.47

Answer: So Abigale can afford an $11,130.47 loan.

Note: Abigail will pay a total of $12,000 ($200 per month for 60 months) to the loan company. The difference between the amount she pays and the amount of the loan is the interest paid. In this case, Abigale is paying $12,000 - $11,130.47 = $869.53 interest total.

You can also use TVM Solver to do this calculation.

Example 10B - TVM Solver

Repeat Previous Example Using TVM Solver

Abigale can afford $200 per month as a car payment. If she can get an auto loan at 3% interest for 60 months (5 years), how expensive of a car can she afford (in other words, what amount loan can Abigale pay off with $200 per month)?

Solution: In this example, we are looking for PV, the starting amount of the loan.

N = 12*5

I% = 3

PV = this is what you are solving for

PMT = -1200

FV = 0

P/Y = 12

C/Y = 12

PMT: END

Once all of the given parameters are entered in, solve for PV to get PV = 11,130.47153

Answer: So Abigale can afford a car loan of up to $11,130.47.

Example 11

You want to take out a $140,000 mortgage (home loan). The interest rate on the loan is 6%, and the loan is for 30 years. How much will your monthly payments be?

Solution: Use the TVM Solver

N = 12*30

I% = 6

PV = 140,000

PMT = this is what you are solving for

FV = 0

P/Y = 12

C/Y = 12

PMT: END

Once all of the given parameters are entered in, solve for PMT to get PMT = ─839.37073

Answer: So you will make payments of $839.38 per month for 30 years.

Note: You’re paying a total of $302,176.80 to the loan company ($839.38 per month for 360 months). You are paying a total of $302,176.80 ─ $140,000 = $162,176.80 in interest over the life of the loan.

Example 12

(Continued from Example 11)

You want to take out a $140,000 mortgage (home loan). The interest rate on the loan is 6%, and the loan is for 30 years. Your monthly payments are $839.38. How much will still be owed after making payments for 10 years?

Solution: Use the TVM Solver

N = 12*10

I% = 6

PV = 140,000

PMT = ─898.38

FV = this is what you are solving for

P/Y = 12

C/Y = 12

PMT: END

Once all of the given parameters are entered in, solve for FV to get FV = -117,158.50

Answer: So you will still owe $117,158.50 after making payments for 10 years.

Section 3.6 You Try Problems:

A) Janine bought $3,000 of new furniture on credit. Because her credit score isn’t very good, the store is charging her a fairly high interest rate on the loan: 16%. If she agreed to pay off the furniture over 2 years, how much will she have to pay each month?

With loans, it is often desirable to determine what the remaining loan balance will be after some number of years. For example, if you purchase a home and plan to sell it in five years, you might want to know how much of the loan balance you will have paid off and how much you have to pay from the sale.

Remember that only a portion of your loan payments go towards the loan balance; a portion is going to go towards interest. For example, if your payments were $1,000 a month, after a year you will not have paid off $12,000 of the loan balance.

B) You finance a $30,000 car at 2.9% interest for 60 months (5 years). What will your monthly payments be? How much will you still owe on the car after making payments for 2 years?

Note: Be sure to round the monthly payment UP to the nearest cent. Then use this (rounded) value when calculating the amount still owed. Round the amount owed UP to the nearest cent.

3.6 – Answers to You Try Problems

a) She will have to pay $146.89 each month.

b) Monthly payments: $537.73 per month. You will still owe $18,518.61 after 2 years.